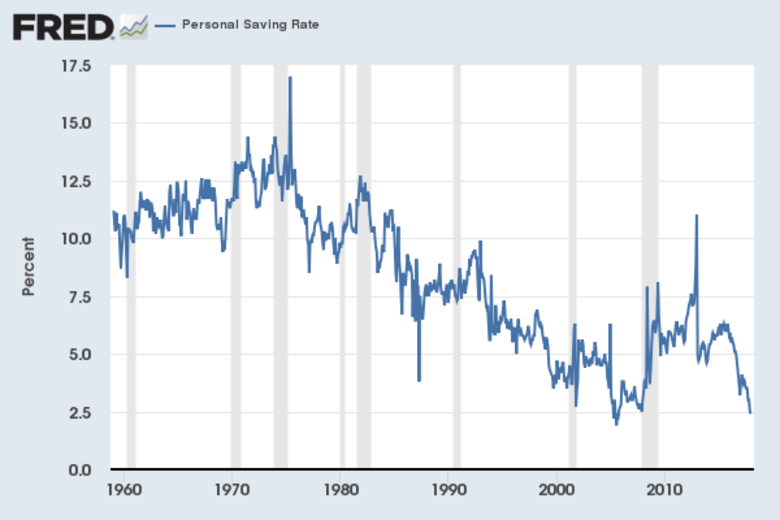

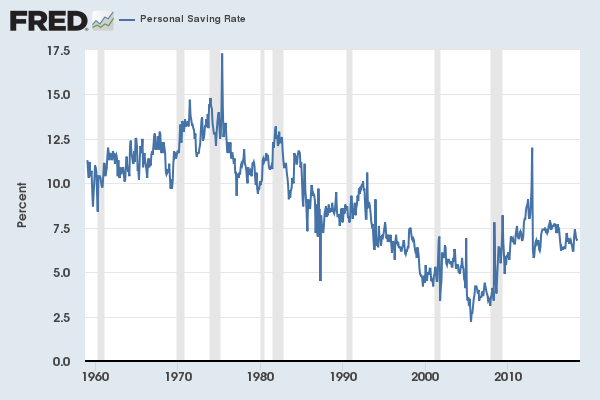

If you were looking for danger signs in the U.S. economy earlier this year, America’s savings habits seemed like one of the few obvious red flags. The personal savings rate had dipped to levels not seen since 2005, a time when households were spending themselves thin and draining their home equity for cash. This seemed like a signal that either consumer spending didn’t have a lot of room to grow, or that if it did, it would be because households were taking on a lot of debt to buy stuff.

It turns out, though, that picture may not have been accurate. Last month, the Bureau of Economic Analysis issued a revised version of its data, which it does from time to time. The new numbers show that the personal savings rate is much higher than perviously thought—as the Wall Street Journal noted Saturday, it jumped to 7.2 percent in the first quarter of 2018, up from the old estimate of 3.3 percent—and that it’s held relatively steady since 2010. Americans, it seems, are still being pretty thrifty, on average.

What made the government change its estimates? It’s worth reading Matthew Klein’s great rundown in Barron’s from a few weeks back. But the basic story is that the IRS realized that Americans were earning slightly more than it previously believed (and, therefore, underpaying their taxes a bit more severely). That helped bump up the country’s overall savings rate, which is calculated by taking all the income individuals take home after taxes, then subtracting interest payments and spending on goods and services.

That sounds like good news for everyone (except tax collectors). But there’s a caveat: As the Journal reports, “Most of the newly discovered income that prompted the BEA’s revisions came in the form of interest, dividends or business owners’ profits, rather than wages.” In other words, a lot of that income may belong to wealthier households, who are stuffing it in their bank accounts. Meanwhile, middle class families may not be saving much more than previously thought.

Correction, Aug. 20, 2018: This post originally misstated that the Wall Street Journal article was published Monday.

Jordan Weissmann is Slate’s senior business and economics correspondent.